Tata Consumer’s Premium GT Expansion with Xpert

Background

Tata Consumer Products is one of India’s oldest and most trusted FMCG brands, carrying the legacy of the Tata name — a name that Indian households have relied on for generations. From kitchens to dining tables, Tata Consumer has built an unmatched presence across the country through brands that millions reach for without a second thought. Their portfolio spans the full spectrum of consumer needs: value-for-money essentials like Tata Salt and Tata Tea that are staples in virtually every Indian home, alongside a rapidly growing range of premium offerings like Tata Soulfull, a millet-based health food brand redefining the wellness category, and Organic India, known for its commitment to organic, sustainably sourced products. This breadth of assortment — from everyday essentials to premium wellness — gives Tata Consumer a unique position in the Indian market, but also introduces a distinct distribution challenge: ensuring the right products reach the right stores.

Challenge Faced

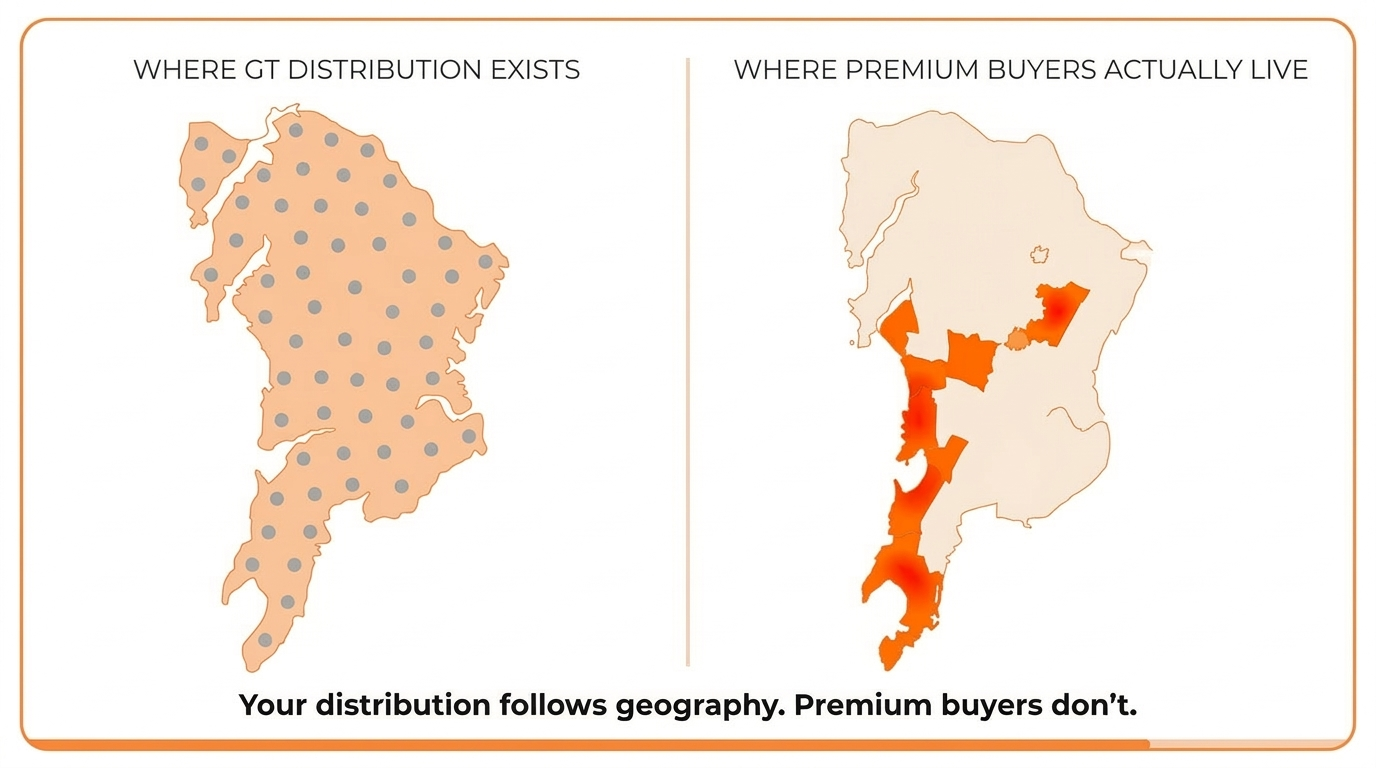

Tata Consumer Products’ premium brands — Tata Soulfull and Organic India — were experiencing strong demand in modern trade and ecommerce, but General Trade distribution remained largely untargeted. The existing GT expansion approach was distributor-led and coverage-driven, stocking outlets based on distributor reach and relationship networks rather than actual buyer demand. This created a fundamental mismatch: premium products like millet cereals and organic wellness products were placed in stores that didn’t serve premium buyer catchments, while high-potential outlets in affluent, buyer-dense pockets remained unstocked. In cities as large and heterogeneous as Mumbai and Delhi, blanket coverage meant significant waste — both in stocking costs and in missed availability where it mattered most. The sales team needed a way to identify which specific GT stores deserved premium SKU allocation and which did not.

Xpert's Strategy Undertaken

Xpert deployed a four-layer intelligence approach across Mumbai and Delhi. First, Xpert mapped the complete GT store universe category-wise — classifying outlets as pan-beedi shops, small kiranas, large kiranas, family convenience stores, supermarkets, and other formats. Second, using verified transaction data from 1,000+ consumer brands, Xpert identified where premium category buyers were physically concentrated — pincode by pincode, cluster by cluster. Third, Xpert overlaid these buyer density maps onto the GT store landscape, isolating outlets that fell within high-premium-buyer catchments. Finally, using store images and AI-powered capability analysis, Xpert evaluated each store’s suitability — assessing frontage, shelf space, store size, and product category fit — to filter out only the stores capable of supporting Tata Consumer’s premium product placement. The result was a prioritised shortlist of demand-validated, capability-verified GT outlets.

Results Achieved

The analysis revealed significant misalignment between Tata Consumer Products’ existing GT footprint and actual premium buyer concentration. Xpert flagged three critical findings: high buyer-density pockets with weak product availability, over-distributed low-premium areas consuming resources without proportionate returns, and territories where further expansion made little commercial sense. Armed with this intelligence, the sales team shifted focus away from distributor-comfortable territories toward buyer-dense zones that were previously underserved. Distribution transformed from a coverage metric into a demand-capture strategy. Premium SKUs were redirected to stores with verified buyer proximity and the physical capability to merchandise them effectively, ensuring that every stocking decision was backed by both demand signals and store readiness rather than distributor convenience or geographic habit.

Inferences & Insights

This engagement reinforces a critical truth about GT distribution in India: coverage does not equal commercial relevance. In metro markets like Mumbai and Delhi, premium buyer concentrations are highly uneven — yet most brands distribute as if demand is evenly spread. Tata Consumer Products’ shift from distributor-led expansion to buyer-backed store selection demonstrates that the intelligence layer between “where stores exist” and “which stores matter” is where distribution ROI is won or lost. For any FMCG brand pursuing premiumisation through General Trade, the lesson is clear: store selection must start from verified buyer presence, not from distributor networks or geographic assumptions. Brands that treat GT expansion as a demand-capture exercise rather than a coverage exercise will consistently outperform those operating on legacy distribution logic.

Xpert helped Tata Consumer Products move beyond distributor-led GT expansion to a demand-driven distribution strategy for premium brands like Tata Soulfull & Organic India — identifying high-potential stores in Mumbai and Delhi through verified buyer intelligence and AI-powered store analysis.

Want results like this for your brand?

Schedule a Demo